Chart Patterns Course – Chapter 1 of 10. Before you learn flags, triangles, or head and shoulders, you need a clean definition of what a chart pattern actually is. That sounds obvious until you realise most pattern education begins by showing the shape after the move worked. At that point you are no longer learning analysis. You are learning archaeology.

What A Chart Pattern Is

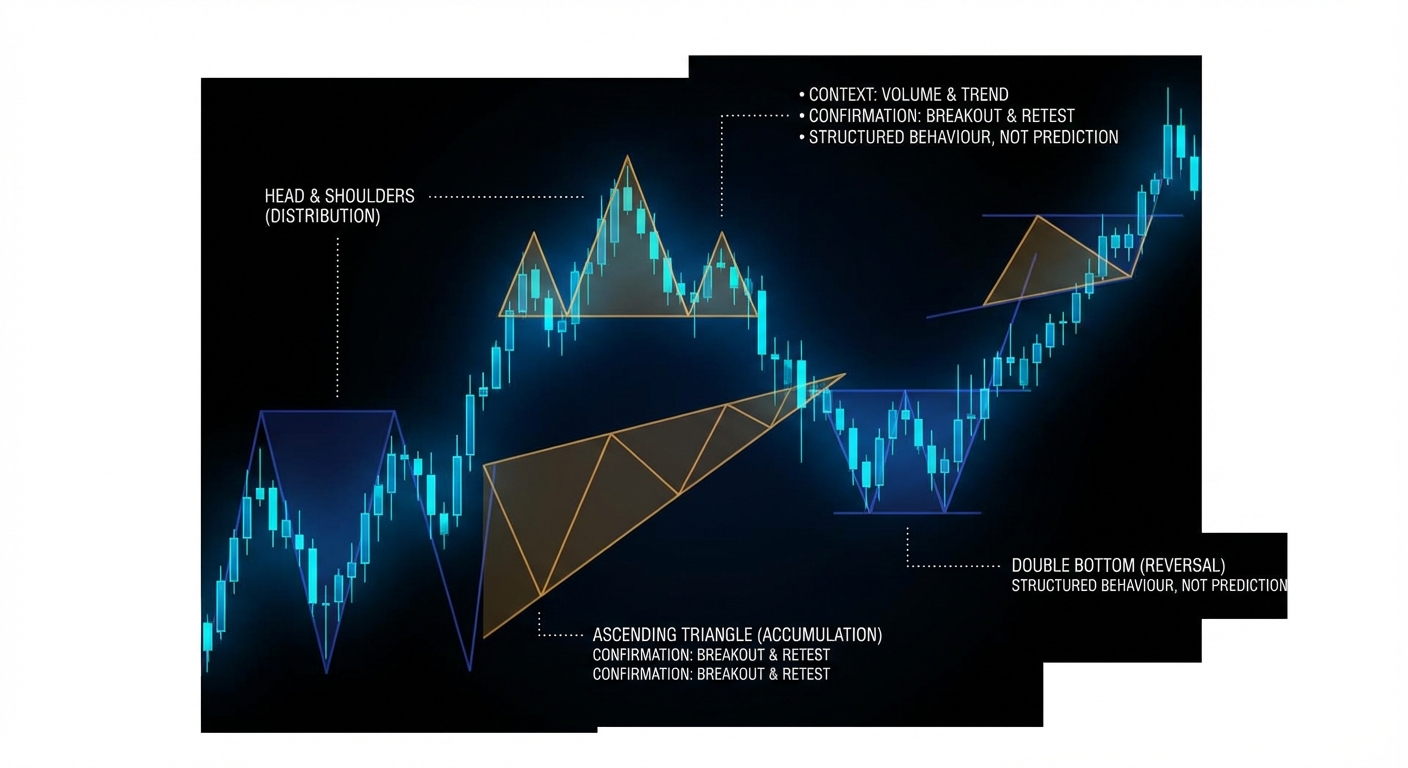

A chart pattern is a recurring price structure that traders use to describe balance, imbalance, continuation, or reversal in a market. That definition matters because it keeps the subject grounded. A pattern is descriptive before it is predictive. It summarises how price moved, where it hesitated, where it failed, and where control may be shifting. A triangle is not a mystical force field. A double top is not a commandment. They are compact visual descriptions of crowd behaviour.

This is also why patterns remain popular. Human beings are very good at recognising structure in incomplete information. Markets generate streams of incomplete information. The temptation to draw meaning out of shape is almost irresistible. Daniel Kahneman would probably call this a perfect factory for overconfident intuition: the chart gives you just enough order to feel certain, even when the evidence is only conditional. That does not make chart patterns useless. It means they need rules, context, and humility.

The Real Academic Claim

Serious research on chart patterns does not say, “all these shapes work.” The strongest careful claim is much smaller and much more useful. Andrew Lo, Harry Mamaysky, and Jiang Wang tried to formalise technical analysis by turning pattern recognition into something computational rather than purely subjective. Their result is still one of the best starting points for anyone who wants evidence instead of campfire stories.

“over the 31-year sample period, several technical indicators do provide incremental information and may have some practical value.” – Lo, Mamaysky, and Wang, Foundations of Technical Analysis

Notice the wording. Incremental information. Some practical value. That is the grown-up version of the subject. It does not promise easy profits. It does not tell you to buy every breakout. It tells you that some recurring structures shift the distribution of outcomes enough to be worth studying. That is a different proposition from folklore, and a far more defensible one.

Why Subjectivity Is the Main Problem

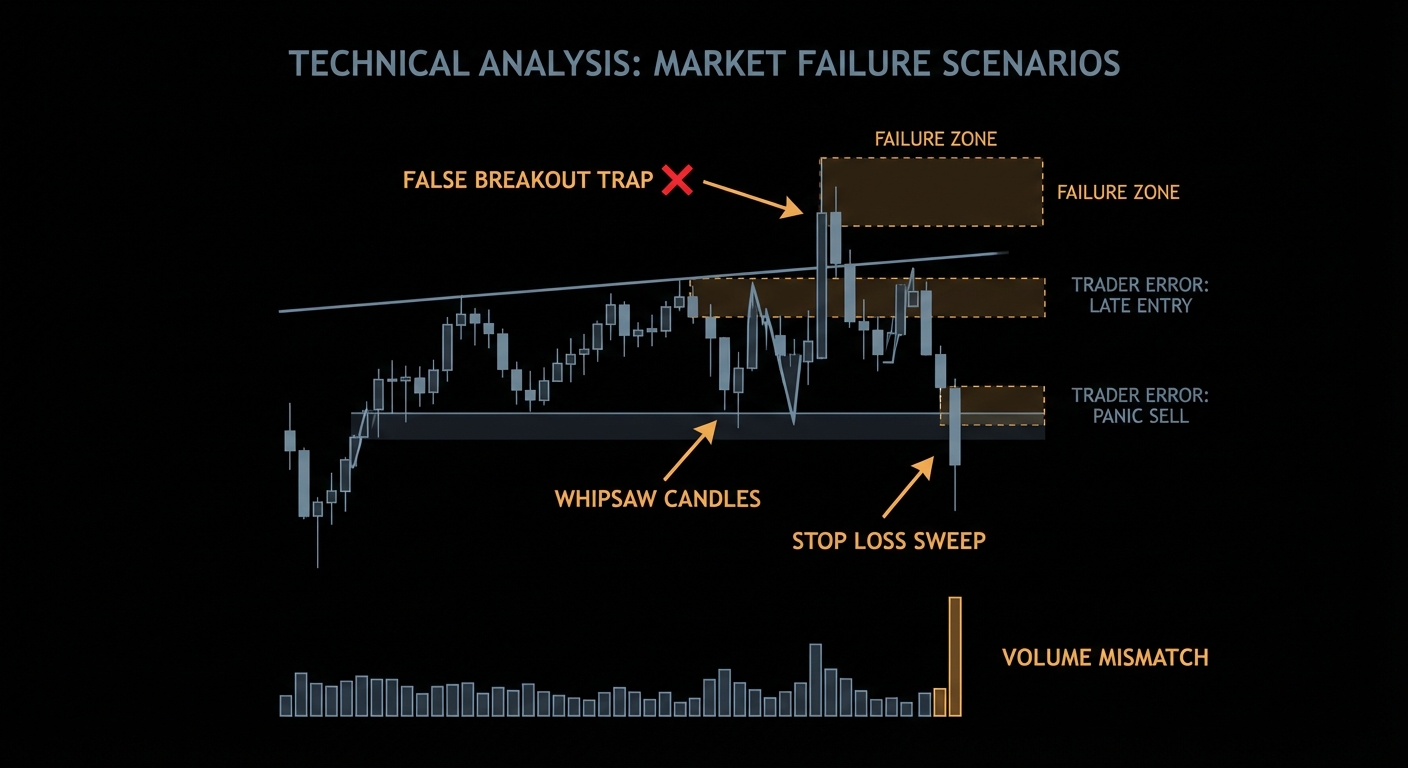

The biggest weakness in chart-pattern education is not that charts are visual. It is that the rules are often vague enough to absorb hindsight. If five traders can draw five different necklines on the same head and shoulders, then the pattern is not yet operational. If the pattern is only obvious after the move reaches the target, then it is not teaching you to trade, it is teaching you to narrate what already happened.

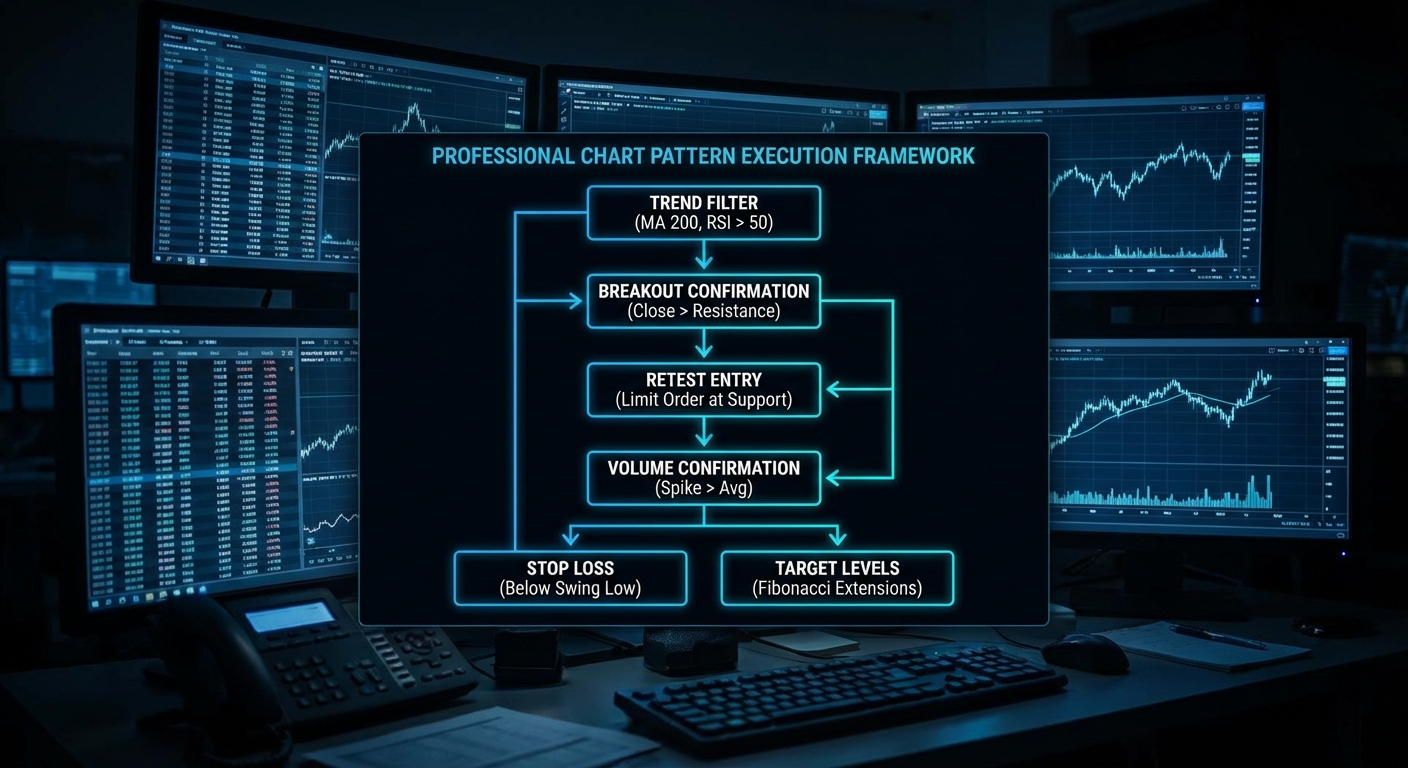

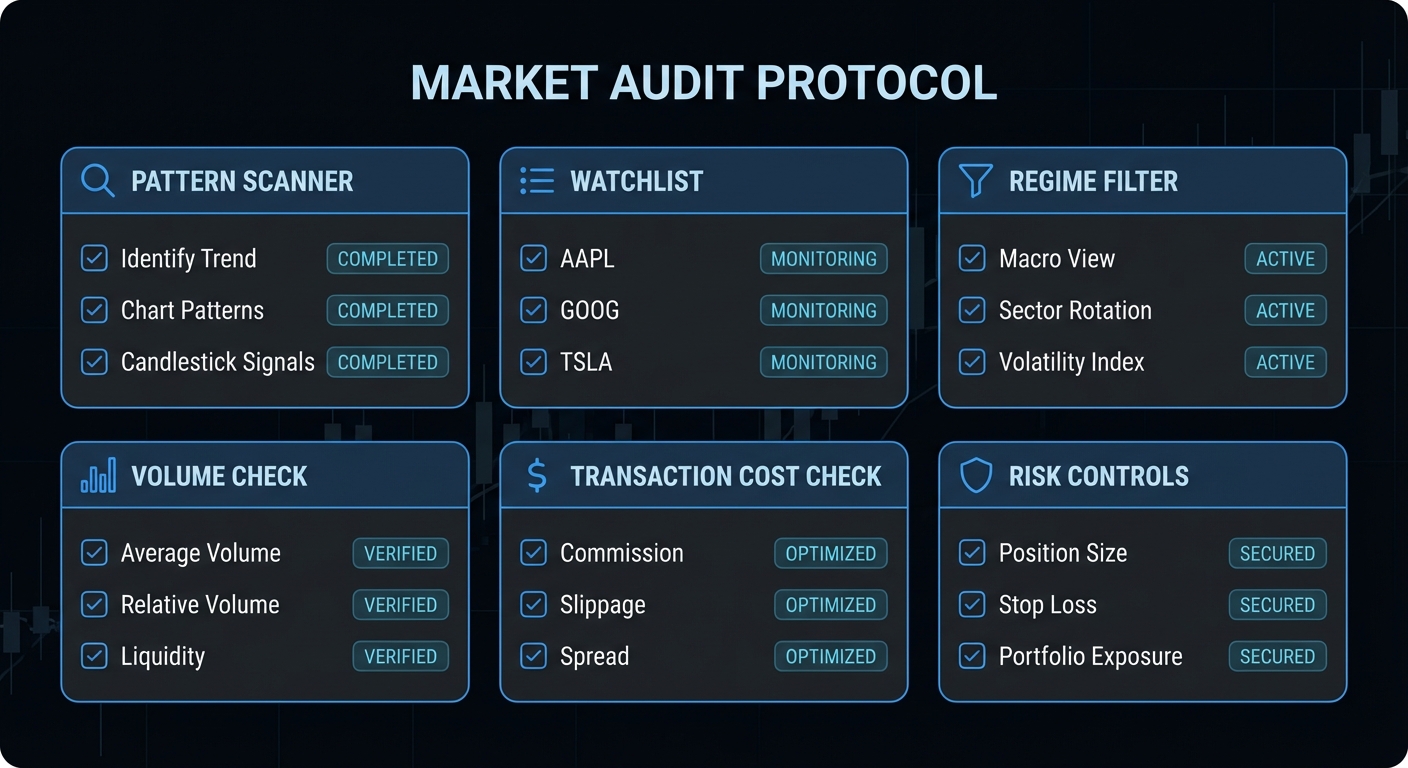

That is why this course treats pattern recognition as a rules problem. You need answers to simple questions: What prior trend is required? What pivots define the structure? What counts as confirmation? Where is the pattern invalidated? What timeframe is relevant? What costs are assumed? Without those answers, the pattern is just a story generator with a candlestick habit.

# Bad pattern logic

if "looks like a triangle":

buy()

# Better pattern logic

if prior_trend_up and range_contracting and close > resistance and invalidation_defined:

buy()That tiny shift in language matters. It moves the pattern from shape worship to conditional decision-making. The first version is a vibe. The second version is a hypothesis that can be tested.

Why Patterns Survive Anyway

Chart patterns survive for three reasons. First, markets do produce recurring structures because humans respond to gains, losses, regret, and crowd behaviour in recurring ways. Second, many participants do watch the same levels, which means some pattern behaviour can become partially self-reinforcing. Third, patterns are genuinely useful for organising trade location and risk. Even when a pattern does not provide a large standalone edge, it can still help define a trigger, an invalidation point, and a reward-to-risk framework.

This is where classic technical-analysis texts still matter. John Murphy and Edwards and Magee remain useful for vocabulary and taxonomy. They help describe what traders mean by reversal, continuation, neckline, support, and measured move. They are not enough as empirical proof on their own, but they remain useful because a course still needs a language. The mistake is confusing the existence of a language with the existence of a guaranteed edge.

What Not To Claim

If you want to stay intellectually honest, avoid three bad claims. First: do not say patterns “always work” in liquid markets. They do not. Second: do not say every false breakout is deliberate manipulation. Sometimes it is simply poor follow-through in a noisy auction. Third: do not present a single success rate as if it applies across assets, regimes, and execution styles. A daily chart breakout in an index future and a one-minute crypto wedge on a thin Sunday book are not the same animal.

Carol Osler’s work on support and resistance is a good warning against simplistic thinking. Her research gives serious support to the idea that technician-used levels can matter, particularly in FX, but it does not give you permission to turn every hand-drawn line into divine revelation. The adult version of technical analysis is conditional, market-specific, and implementation-aware.

How To Think About Patterns From Here

The cleanest mental model is this: patterns are compact maps of auction behaviour. Some show compression inside trend. Some show repeated failure at extremes. Some show exhaustion after a directional move. Their value comes from combining structure with context, confirmation, and risk logic. Used that way, they are useful. Used as free-floating shapes, they become one more way the market sells certainty to people who desperately want it.

Summary Takeaway

Chart patterns are best treated as structured hypotheses about market behaviour, not as magical predictors. The evidence supports modest informational value in some cases, but only when definitions, context, confirmation, and execution are handled with discipline.

Course Navigation

Next: Market Structure for Chart Patterns: Trend, Support, Resistance, and Volume

Full course: Chart Patterns Course – Evidence, Execution, and Risk

This chapter is part of the Chart Patterns Course.